How Shopify Store Credit Payouts Work (and Why They're Genius for Affiliate Programs)

Paying affiliates with Shopify store credit instead of cash can increase repeat purchases and simplify your payout logistics.

Calvin

Buzzbassador

Most Shopify brands think about affiliate payouts like this: "You bring in sales, we send you money via PayPal."

That works. But it's only half the opportunity.

Every time you send cash to an affiliate, money leaves your business and disappears into the economy. Your affiliate spends it at Starbucks, Target, or a competitor's store. The transaction is complete. The relationship becomes purely transactional.

Comparison of cash payouts versus store credit payouts for affiliate programs showing money leaving forever versus revenue returning to brand

Store credit payouts work differently. When you pay affiliates in store credit, every payout turns into a new order. Your best promoters become repeat customers. They try more of your catalog, create more content, and build deeper connections to your brand. The money you spend on affiliate rewards comes back as revenue instead of vanishing as an expense.

This isn't about being cheap with your partners. It's about designing a program where everyone wins: affiliates get more value, you keep revenue inside your ecosystem, and the relationship compounds instead of ending at checkout.

Here's how Shopify store credit payouts actually work, when to use them versus cash, and how to automate both with Buzzbassador using payout rules, PayPal integration, and Reward Processing Periods.

The Problem with Cash-Only Affiliate Payouts

Let's be honest about what happens when you only pay affiliates in cash.

You track sales. Your affiliate generates $1,000 in revenue. You calculate their 10% commission ($100). You send it to their PayPal. Done.

But here's what actually just happened: You spent $100, that money left your business forever, your affiliate has zero reason to shop with you again, they might use that cash at a competitor, you missed an opportunity to deepen the relationship, and the entire interaction was purely transactional.

Six months later, that same affiliate has never made a single purchase from your store. They promote you when commissions are good, but they're not actually customers. They don't wear your products. They don't genuinely use them. Their content feels generic because they're not personally invested.

Now imagine a different scenario: Same affiliate generates $1,000 in revenue. You give them $150 in store credit instead of $100 cash. They browse your catalog and find three products they've been eyeing. They place an order. Two weeks later, they're wearing your hoodie in an Instagram story. A month later, they're back for another order, this time paying partially with their own money.

That's the difference. One approach treats affiliates as contractors. The other treats them as customers who happen to be excellent at marketing.

What Are Shopify Store Credit Payouts?

Store credit means paying your affiliates with value they can only spend at your store. Instead of sending $50 to their PayPal, you give them $75 in credit to spend on your products.

With Buzzbassador's Shopify Store Credit integration, the process is seamless. When you pay a reward with store credit, that amount is added directly to the member's customer account in your Shopify store. They log in with the same email they use for Buzzbassador, add items to their cart, and see store credit as a payment option at checkout. No codes to copy, no gift cards to manage—it's automatically available in their Shopify account.

Buzzbassador handles the commission calculation and tracking. After a creator makes a sale, Buzzbassador tracks it, calculates their reward, moves it from Pending to Due after your Reward Processing Period (the waiting period for returns and refunds), and then you approve the payout. When you choose to pay with store credit, Buzzbassador sends that amount to the member's Shopify customer account where they can redeem it at checkout.

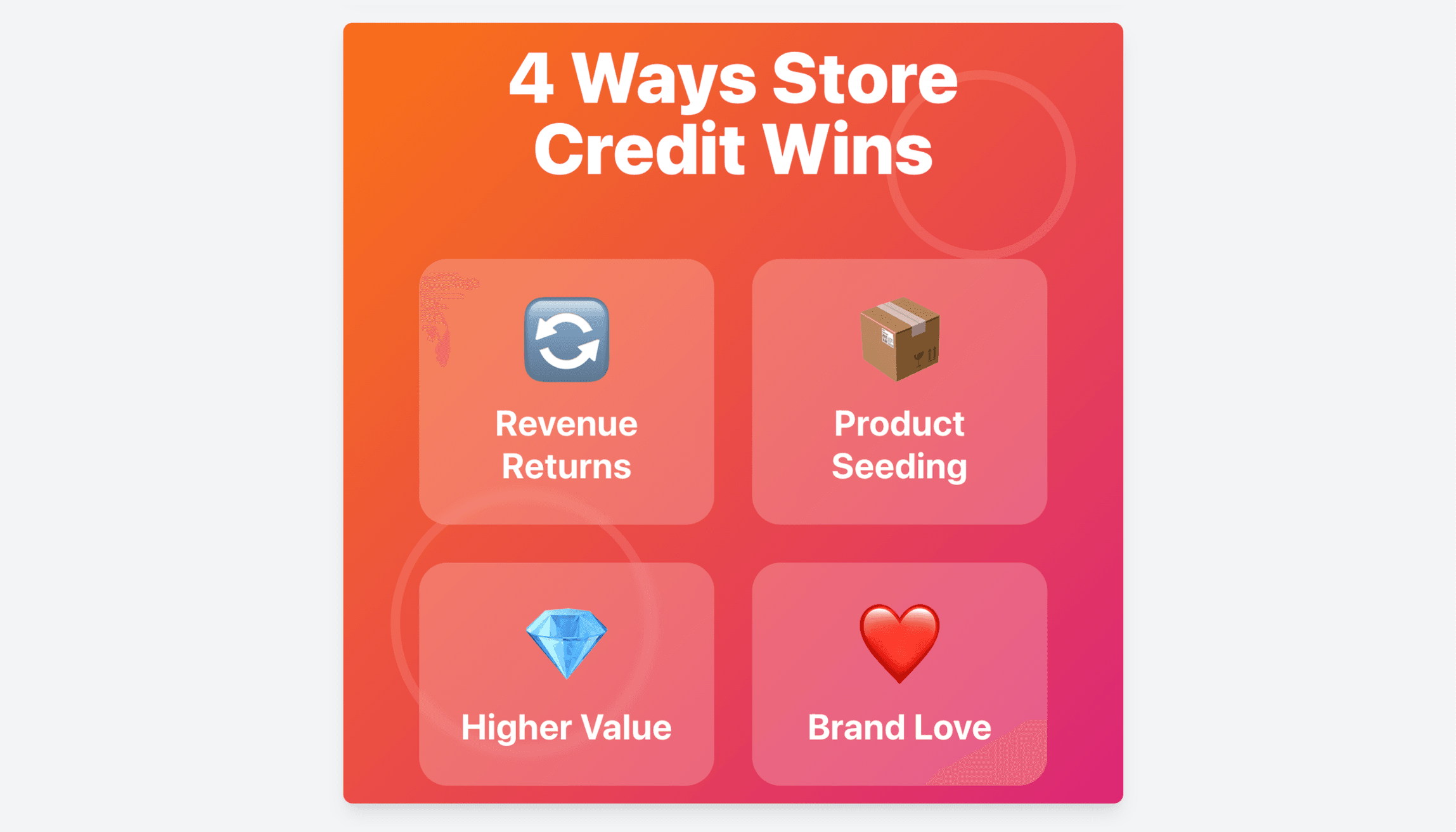

Why Store Credit Payouts Work Better Than Cash

Store credit isn't just another payout type. It fundamentally changes the economics of your affiliate program in four specific ways.

1. It Keeps Value in Your Brand Ecosystem

With cash payouts, money leaves your business and affiliates spend it anywhere. With store credit payouts, rewards come back as new orders. You get repeat purchases from people who already love your brand. Affiliates end up trying more of your catalog, which generates even more content and referrals.

You're turning affiliate rewards into future revenue instead of pure cost. The payout doesn't end the relationship—it extends it.

Think about the lifetime value impact. A cash-only affiliate might promote your brand for three months, earn $500 total, and never place an order. Their customer lifetime value to your business is zero dollars despite generating thousands in revenue. A store credit affiliate who earns that same $500 in credit will likely spend it across multiple orders, try different product categories, and develop preferences. Some will even spend beyond their credit balance using their own money. Their lifetime value might be $300, $500, or more—not zero.

2. Higher Perceived Value at Lower Actual Cost

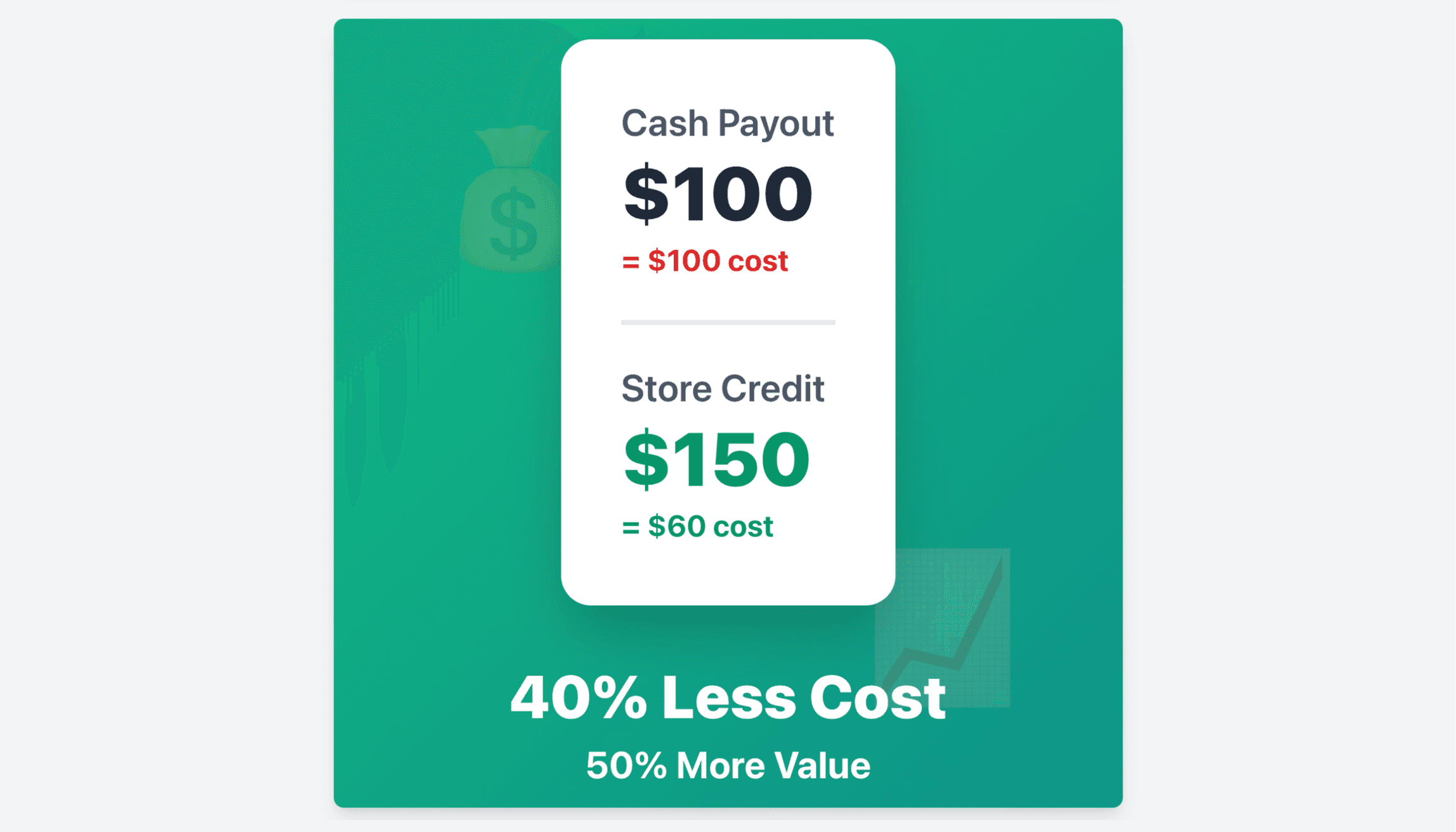

Because store credit is redeemed as product, you can offer more credit than you'd pay in cash. Your affiliates feel like they're getting a better deal (receiving $100 in product versus $60 in cash), but your actual cost is your product margin, not the full retail amount.

Here's the math: if your margin is 60%, giving $100 in store credit costs you $40 in real expense. That same creator might be perfectly happy with $60 in cash—or thrilled with $100 in product. You've increased their perceived value by 67% while spending 33% less than the cash equivalent.

Let's make this concrete with real numbers. Say you run a Shopify apparel brand. Your average hoodie retails for $65 and costs you $26 to produce and fulfill (60% margin). An affiliate generates $1,000 in sales.

Cash payout scenario: 10% commission equals $100 cash to PayPal. Your cost is $100. Affiliate's purchasing power is $100 anywhere.

Store credit scenario: You offer $150 in store credit instead. Your actual cost is $60 in product margin (assuming they spend it all). Affiliate's purchasing power at your store is $150 in retail value.

The affiliate gets 50% more value. You spend 40% less. Both sides win, and the affiliate is now wearing your products, which leads to more organic content and more sales.

3. Built-In Product Seeding and Content Fuel

When affiliates are paid in store credit, they naturally try new collections and product categories, post more unboxing, haul, and try-on content, and show how your products fit into their everyday life.

You're seeding product with people who already sell for you, which is more efficient than running a separate seeding program. Every payout becomes content fuel. Every redemption becomes a potential post.

Most brands spend thousands on separate influencer seeding campaigns. You send product to creators. Some post about it. Many don't. You have no way to track ROI because there's no direct sales attribution. Store credit payouts solve this elegantly. You're only "seeding" product to people who've already proven they can drive sales. The credit they earn is directly tied to their performance. When they redeem that credit and receive products, they're more likely to post about them because they're already active promoters of your brand.

4. Stronger Brand Affinity and Emotional Connection

Store credit subtly shifts the dynamic from "contractor getting paid" to "superfan getting hooked up." Affiliates who are consistently rewarded in store credit wear and use your products more often, have more to show and talk about, and feel more like part of the brand instead of just another partner.

That emotional connection translates into better quality content and higher lifetime performance. They're not just promoting your products—they're living with them. This is the difference between someone who says "Here's a discount code for a brand I work with" versus "I'm obsessed with this brand—here's my code." The first is a transaction. The second is a recommendation. Audiences can tell the difference.

When to Use Cash Versus Store Credit (and When to Mix Both)

The smart move isn't picking cash or credit forever. It's choosing the right payout type for the right scenario.

When Store Credit Works Best

Store credit is especially powerful when you're working with micro-influencers, ambassadors, or community members who care about your brand, your goal is brand love, content, and retention rather than just one-time sales, your average order value and margins make credit feel generous, or you're building tiered programs where early tiers earn product and higher tiers earn cash.

Community-driven programs are perfect for store credit. If you're building a program around brand fans, college ambassadors, or local advocates, these people already want your products. Giving them credit to get more of what they love is a natural fit.

Content-first campaigns work beautifully with store credit. When your primary goal is generating user-generated content rather than pure performance, store credit keeps costs low while building your content library. You might offer $100 in credit for posting three approved videos. The creator gets products to use in future content, and you get the posts you need.

New ambassador onboarding is ideal for store credit rewards. New ambassadors don't know if they'll perform well yet. Starting them with store credit rewards lets them build a relationship with your brand before they earn significant cash. If they're good promoters, you can graduate them to cash later.

When Cash Payouts Make Sense

Cash still wins when you're working with professional creators and influencers who expect monetary compensation, you're running performance-heavy campaigns with strict ROAS or CPA goals, or you're negotiating custom deals with higher-volume partners.

Professional influencer partnerships require cash. If you're paying someone with 100K+ followers for a dedicated post or campaign, they expect cash. Store credit won't work here unless you're also a luxury brand they personally love.

High-volume partners need cash. Your top performer drives $50,000 in monthly revenue and earns $5,000 in commissions. That's their income. They need cash, not store credit. Even if they love your products, they can't pay rent with store credit.

This is where Buzzbassador's PayPal integration comes in. The platform tracks affiliate-generated revenue, calculates rewards based on your rules, moves them from Pending to Due after your Reward Processing Period, and then you can pay those rewards via PayPal in just a couple of clicks.

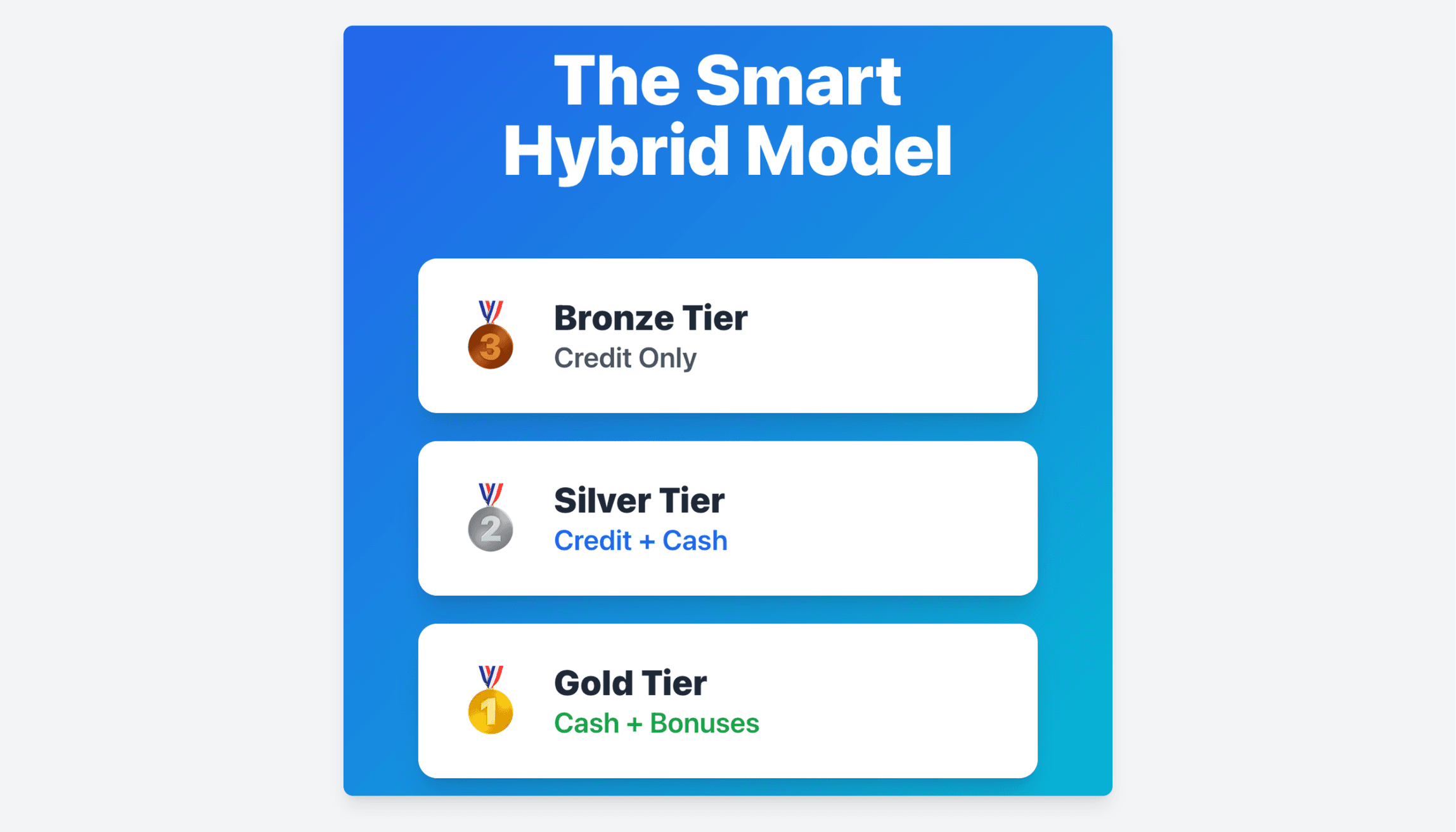

The Hybrid Model (Often the Best Approach)

Many high-performing programs use both payment types. Lower tiers earn store credit only. Mid tiers get a mix of store credit plus cash. Top tiers receive mostly cash with optional store credit bonuses.

Three-tier hybrid affiliate program structure showing Bronze credit-only, Silver credit plus cash, and Gold cash-focused tiers

Tier 1 (Bronze) could be store credit only. Affiliates in this tier earn 10% of sales in store credit with a minimum $25 payout threshold. This tier is perfect for new ambassadors, casual promoters, and community members.

Tier 2 (Silver) could be a hybrid split. Once an affiliate hits $500 in total sales generated, they move to Silver. First $100 per month in commissions goes out as store credit at a 15% rate, and anything above $100 gets paid as cash via PayPal at 12%. This structure encourages them to keep trying new products while rewarding higher performance with real money.

Tier 3 (Gold) could be cash-first with credit bonuses. Top performers earning $2,000+ in monthly sales get 15% cash commissions via PayPal as their base. You can layer in store credit bonuses for specific campaigns, new launches, or hitting stretch goals.

How Buzzbassador Powers Smart Payout Rules on Shopify

Buzzbassador is built for Shopify brands that want to track, reward, and scale affiliate and ambassador programs without manual spreadsheets or one-off payments. Here's how it handles payouts.

Track Rewards from Pending to Due to Paid

When an affiliate makes a sale, Buzzbassador automatically calculates their commission and adds it to their Pending balance. This is where the Reward Processing Period comes in—your setting for how many days rewards stay Pending before they become Due (payable).

This waiting period protects you from paying out on orders that get returned or refunded. You might set 7 days for low-return items, 21 days for most products, or 30 days for categories with higher return risk. After that period passes and the order is still valid, the reward automatically moves from Pending to Due.

When rewards are Due, you see them on your Rewards page in Buzzbassador. You can then approve payouts in batches. Choose whether to pay via Shopify Store Credit, PayPal, Tremendous (gift cards), or mark as paid externally if you're handling payment outside the platform (like via ACH, Cash App, or Venmo).

Set Commission Structures Per Program

Programs in Buzzbassador control how affiliates earn commissions. You might create a "College Ambassadors" program with 15% commission rates and a "Pro Influencers" program with 12% rates. You can set different commission percentages per program, and configure a Reward Processing Period and minimum payout threshold that match your overall payout policy.

Then, when it's time to actually pay rewards, you decide on the Rewards page whether those specific rewards get paid as store credit or cash. This gives you flexibility to pay different programs differently in practice (always use store credit for Program A rewards, always use PayPal for Program B rewards), even though the payout method choice happens at payout time rather than being locked into the program settings.

Pay Rewards in Just a Few Clicks

Buzzbassador doesn't automatically fire payouts on a schedule because PayPal and other payout methods require human authorization. But it makes the approval process incredibly fast.

Once rewards move from Pending to Due, you go to your Rewards page, select the rewards you want to pay (you can filter by program, affiliate, or date), and click Pay. Choose your payout method—Shopify Store Credit, PayPal, or Tremendous. For store credit, Buzzbassador sends the amount to each member's Shopify customer account. For PayPal, it processes the cash payment. You can pay dozens or hundreds of affiliates in one batch with just a couple of clicks.

Example Payout Strategies You Can Run with Buzzbassador

Here are real-world structures you could set up today.

Strategy 1: Ambassador Launch Program (Store Credit-Focused)

Create a program for new ambassadors with 15% commission on sales. Set your Reward Processing Period to 21 days and minimum payout threshold to $50. When rewards become Due, pay them all via Shopify Store Credit. Your goal is turning fans into repeat customers and product showrooms. New ambassadors get rewarded generously while you build long-term relationships and generate consistent content.

Strategy 2: Hybrid Growth Tier (Credit Plus Cash)

Target mid-tier performers with a program offering 15% commission. Set a 21-day Reward Processing Period. When their rewards become Due each month, pay the first $100 as store credit and anything above that via PayPal. Your goal is encouraging them to keep trying new products while still paying meaningful cash as they scale.

Strategy 3: Pro Creator Tier (Cash-Focused with Occasional Credit)

Build this for top performers with 15% commission via PayPal as the base. If your refund policy allows it, you might set a shorter Reward Processing Period (for example, 14 days) and process payouts via PayPal. Occasionally, when you launch new products or run seasonal campaigns, offer store credit bonuses on top of their regular cash commissions. Your goal is competitive compensation plus strategic product seeding.

Strategy 4: Content-Based Store Credit Rewards

Instead of tying everything to sales, reward specific content creation with store credit. Approve three Instagram Reels and earn $100 in store credit. Create a YouTube review and earn $150 in credit. This approach works when you need consistent content more than pure sales performance. You're paying for content in products rather than cash, which keeps costs low while building your content library.

Common Mistakes to Avoid with Store Credit Payouts

Store credit programs can backfire if you structure them poorly. Here are the mistakes that sink programs and how to avoid them.

Mistake 1: Making Store Credit Feel Like a Downgrade

The mistake is offering store credit to affiliates who were expecting or previously earned cash. They feel like you're cheapening the relationship or cutting their compensation.

The fix: Position store credit as additional value, not a replacement. If you're transitioning from cash to credit, increase the percentage to maintain or increase perceived value. Frame it as "We're giving you more value through products" rather than "We're cutting your cash." Better yet, offer both and let affiliates choose their preference.

Mistake 2: Setting Thresholds Too High

The mistake is setting a $200 minimum payout threshold because you don't want to process small amounts frequently. Most micro-ambassadors never hit $200 in commissions. They promote for months, accumulate $75 in earnings, realize they'll never reach the threshold, and quit.

The fix: Keep minimum thresholds reasonable—$25 to $50 is ideal for most programs. Yes, you'll process payouts more frequently, but you'll keep affiliates engaged and motivated. Batch process payouts monthly to manage frequency.

Mistake 3: No Clear Redemption Communication

The mistake is that affiliates earn store credit but don't understand how to use it. They don't realize it's automatically in their Shopify account. They think they need a code. The process feels unclear.

The fix: Send a clear email when you issue store credit. Explain that the credit is now in their Shopify customer account and will automatically appear as a payment option at checkout when they log in with their registered email. Include a direct "Shop Now" link. Make redemption feel simple and exciting.

Mistake 4: Forgetting About Margins

The mistake is offering generous store credit percentages (25%+) without doing the margin math. Affiliates redeem credit for high-value, low-margin products. Your program becomes unsustainable.

The fix: Know your margins by category. If certain products have terrible margins, consider excluding them from store credit redemption or calculating commissions differently. Alternatively, guide affiliates toward higher-margin products by featuring them prominently in redemption communications.

Turn Affiliate Payouts into Customer Retention with Buzzbassador

If your affiliate or ambassador program only pays in cash, you're leaving retention and repeat revenue on the table.

With Shopify store credit payouts, you keep more value in your brand ecosystem, turn ambassadors into repeat customers, seed more product and generate more content, and make your program feel generous without destroying margins.

With Buzzbassador, you can pay rewards via Shopify Store Credit or PayPal depending on what makes sense for each program, set commission structures that match your strategy, and configure a Reward Processing Period that aligns with your refund window.

Every payout becomes an opportunity to deepen the relationship instead of ending it. Every reward keeps working for your brand instead of disappearing into the economy. Your affiliates get more value. You keep more revenue. The relationship compounds instead of ending at checkout.

👉 Turn affiliate payouts into customer retention with Buzzbassador.